Maui Real Estate Market Update COVID-19

Posted by Alex Cortez on Thursday, April 9th, 2020 at 3:30pm.

First and foremost, our thoughts and prayers to those most significantly affected by COVID-19 and the on-going pandemic crisis.The health and well-being of our clients and staff is of the utmost concern and, at challenging time such as this, that will continue to be our top priority. We continue to service our clients professionally and dutifully, utilizing all available technological tools that enable us to maintain business continuity - from digital signing, to virtual tours (click here for an example), to virtual meetings and more, we are well-positioned to continue. With perseverance, patience, collaboration and Aloha, we are confident that this too shall pass and our community will be stronger than ever.

With that said, we are continuously asked by our clients and customers as to the state of the Maui real estate market, particularly at a time with so much volatility and uncertainty. Our market update below is based on previous months performance and currently available data, any opinion of future performance is (at best) a guesstimate and not guaranteed, nor meant to be relied upon.

As a recap of March:

Single-Family Residences - The median sales price rose to an astonishing $840K, easily beating the mark $712,718 in the same month last year (+17.9%), while the Year-to-Date (YTD) median had a more modest improvement, from $735K to $776,075 (+5.6%). The number of closed sales in March saw a slight decline, from 96 in March 2019 to 89 in March of this year (-7.3%). Keep in mind that the gravity of the COVID-19 crisis became more pronounced towards the end of the month, hence the month as a whole may paint a positive picture that is not reflective of the market slowdown. Better metrics to keep in mind are amount of new listings, whereby 94 (-43%) new listings in March compare poorly to 165 in the same month of the previous year, and the amount of pending sales, decreasing from 112 the previous year to 65 this past month (-42%), both these trends will be relayed in the upcoming months. The largest decreases in March were in Wailuku and Kihei.

Condominiums - The median sales price had a more modest increase than the SFR's, increasing from $508,500 last year to $555K ($9.1) this March, while the YTD increase is from $525K in 2019 to $555K this year (+5.7%). The number of closed sales saw a small uptick, from 154 last March to 159 (+3.2%). In stark contrast to SFR's, new listings actually increased to 173 (+8.8%) last month when compared to same period in previous year. Where the story is more telling is in Pending Sale, where the decrease is staggering: 148 last March compared to 64 this year (-56.8%). To put some context here, many of the condominiums on Maui are second-home, vacation-rental properties that are an investment to owners, so it makes sense that many tried to put on the market in order to cash out, while Buyer demand has decreased on what is arguably a discretionary purchase.

For a full breakdown, view the complete Maui Real Estate - March 2020 Statistics.

With that in mind, where is the market headed? Anecdotally, what we are seeing are Buyers who are expecting deep discounts based on experiences of what the last Recession brought and Sellers who see current conditions as a temporary reprieve from normal market conditions and expect somewhat of a return towards 'normalcy' by the end of summer (some concede that it might be into late year). So far we have not seen decreased values in closed sales - that's not to say that it can't or won't come, but as of right now the value of closed sales is consistent to recent sales. This gap in expectations between Buyers and Sellers is causing negotiations to stall and with the overhanging cloud of uncertainty ("will the current 'Stay at Home' orders be extended throughout the country or end at the end of April), the expectation is that April will be a 'wait and watch' period where neither side wants to make significant moves.

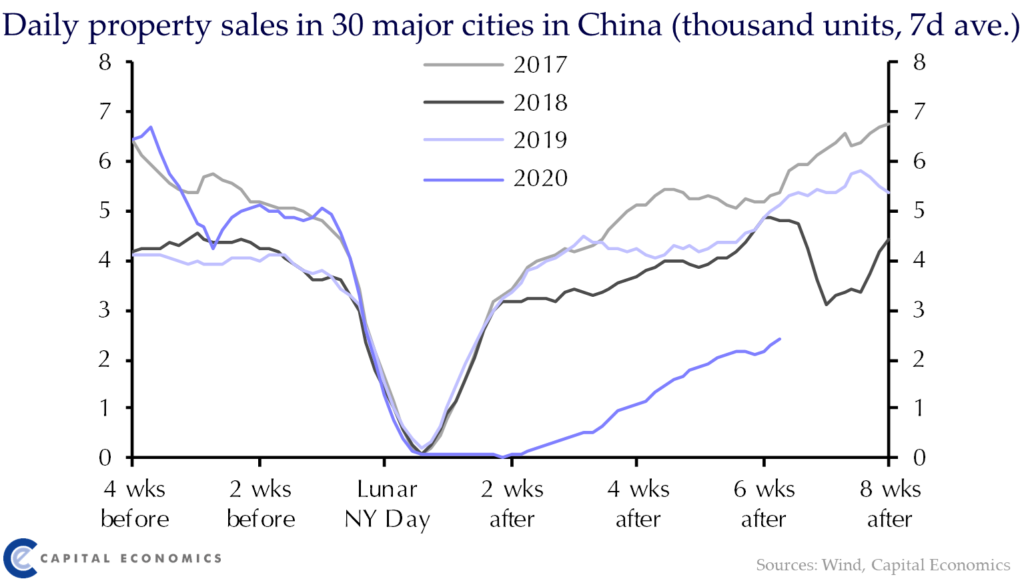

However, we do have the benefit of a blueprint of China's experience, as the Chinese experienced the crisis ahead of what we are going through - of course, keep in mind that in the US we may have a much different COVID-19 pandemic and recovery. So with that, let's take a look at the following chart, as noted on Macrobusiness:

It's worth noting that the Chinese market has a drop annually coinciding with the Lunar New Year Day (LNYD) and in this case the LNYD coincidentally fell at the same time as COVID-19 crisis, whereas our market did not have that upcoming 'pause' - we came to a screeching halt in market activity. As can be ascertained, in previous years market activity decreased two weeks prior to LNYD and returned back to where it left off two weeks past. However, as shown on this chart, sales volume remained relatively unmeasurable until 3 weeks after and at 6 six weeks post LNYD, number of sales was roughly 50% of average of previous two years. On our end, we'll keep watching the China real estate market to see recovery patterns / trends and see if there are parallel patterns on Maui. Updates will be posted.

Projections - and keep in mind, these are opinion-only.

* Residential Owner-Occupied Market - The Housing Affordability Index has been brutal on Maui, with many local families unable to afford the cost of a home, as noted earlier this March the median was $840K. With unemployment in the upcoming months expected to incredibly high (based on heavily hospitality-based economy), the pool of prospective Buyers will likely decrease. With lessen Buyer demand, a downward push on prices may lay ahead.

* Vacation-Rentable Condos - This will be an interesting micro-market to gauge, particularly among differing price points. For many owners, these are income-producing assets but at a time filled with uncertainty, being 'liquid' can be an attractive safety net and we may see an influx of inventory. However, there may be some drastically different conditions based on price (for this sake, we can segment as sub-$500K, $500K to $1M, $1M to $2.5M, and $2.5+). The segments under $1M might be (arguably) more motivated than others in the $1M+ categories where for many these were lifestyle-based purchases.

Again, the above 'projections' are speculative at best and painting in very broad terms, whereas each Seller has very individual and unique circumstances that may differ widely from our projections.

For an in-depth analysis on the Oahu real estate market, contact us. Lastly, with team members on Kauai and the Big Island, we are uniquely poised to provide expert-level information covering the entire State of Hawaii.

With that said, we are continuously asked by our clients and customers as to the state of the Maui real estate market, particularly at a time with so much volatility and uncertainty. Our market update below is based on previous months performance and currently available data, any opinion of future performance is (at best) a guesstimate and not guaranteed, nor meant to be relied upon.

As a recap of March:

Single-Family Residences - The median sales price rose to an astonishing $840K, easily beating the mark $712,718 in the same month last year (+17.9%), while the Year-to-Date (YTD) median had a more modest improvement, from $735K to $776,075 (+5.6%). The number of closed sales in March saw a slight decline, from 96 in March 2019 to 89 in March of this year (-7.3%). Keep in mind that the gravity of the COVID-19 crisis became more pronounced towards the end of the month, hence the month as a whole may paint a positive picture that is not reflective of the market slowdown. Better metrics to keep in mind are amount of new listings, whereby 94 (-43%) new listings in March compare poorly to 165 in the same month of the previous year, and the amount of pending sales, decreasing from 112 the previous year to 65 this past month (-42%), both these trends will be relayed in the upcoming months. The largest decreases in March were in Wailuku and Kihei.

Condominiums - The median sales price had a more modest increase than the SFR's, increasing from $508,500 last year to $555K ($9.1) this March, while the YTD increase is from $525K in 2019 to $555K this year (+5.7%). The number of closed sales saw a small uptick, from 154 last March to 159 (+3.2%). In stark contrast to SFR's, new listings actually increased to 173 (+8.8%) last month when compared to same period in previous year. Where the story is more telling is in Pending Sale, where the decrease is staggering: 148 last March compared to 64 this year (-56.8%). To put some context here, many of the condominiums on Maui are second-home, vacation-rental properties that are an investment to owners, so it makes sense that many tried to put on the market in order to cash out, while Buyer demand has decreased on what is arguably a discretionary purchase.

For a full breakdown, view the complete Maui Real Estate - March 2020 Statistics.

With that in mind, where is the market headed? Anecdotally, what we are seeing are Buyers who are expecting deep discounts based on experiences of what the last Recession brought and Sellers who see current conditions as a temporary reprieve from normal market conditions and expect somewhat of a return towards 'normalcy' by the end of summer (some concede that it might be into late year). So far we have not seen decreased values in closed sales - that's not to say that it can't or won't come, but as of right now the value of closed sales is consistent to recent sales. This gap in expectations between Buyers and Sellers is causing negotiations to stall and with the overhanging cloud of uncertainty ("will the current 'Stay at Home' orders be extended throughout the country or end at the end of April), the expectation is that April will be a 'wait and watch' period where neither side wants to make significant moves.

However, we do have the benefit of a blueprint of China's experience, as the Chinese experienced the crisis ahead of what we are going through - of course, keep in mind that in the US we may have a much different COVID-19 pandemic and recovery. So with that, let's take a look at the following chart, as noted on Macrobusiness:

It's worth noting that the Chinese market has a drop annually coinciding with the Lunar New Year Day (LNYD) and in this case the LNYD coincidentally fell at the same time as COVID-19 crisis, whereas our market did not have that upcoming 'pause' - we came to a screeching halt in market activity. As can be ascertained, in previous years market activity decreased two weeks prior to LNYD and returned back to where it left off two weeks past. However, as shown on this chart, sales volume remained relatively unmeasurable until 3 weeks after and at 6 six weeks post LNYD, number of sales was roughly 50% of average of previous two years. On our end, we'll keep watching the China real estate market to see recovery patterns / trends and see if there are parallel patterns on Maui. Updates will be posted.

Projections - and keep in mind, these are opinion-only.

* Residential Owner-Occupied Market - The Housing Affordability Index has been brutal on Maui, with many local families unable to afford the cost of a home, as noted earlier this March the median was $840K. With unemployment in the upcoming months expected to incredibly high (based on heavily hospitality-based economy), the pool of prospective Buyers will likely decrease. With lessen Buyer demand, a downward push on prices may lay ahead.

* Vacation-Rentable Condos - This will be an interesting micro-market to gauge, particularly among differing price points. For many owners, these are income-producing assets but at a time filled with uncertainty, being 'liquid' can be an attractive safety net and we may see an influx of inventory. However, there may be some drastically different conditions based on price (for this sake, we can segment as sub-$500K, $500K to $1M, $1M to $2.5M, and $2.5+). The segments under $1M might be (arguably) more motivated than others in the $1M+ categories where for many these were lifestyle-based purchases.

Again, the above 'projections' are speculative at best and painting in very broad terms, whereas each Seller has very individual and unique circumstances that may differ widely from our projections.

For an in-depth analysis on the Oahu real estate market, contact us. Lastly, with team members on Kauai and the Big Island, we are uniquely poised to provide expert-level information covering the entire State of Hawaii.

Specializing in Makena and Wailea real estate, Alex Cortez is fully dedicated to representing his clients ethically and diligently. Contact him at 808.385.5034 or Alex@MauiRealEstateSearch.com for more information.